[3 min read, open as pdf]

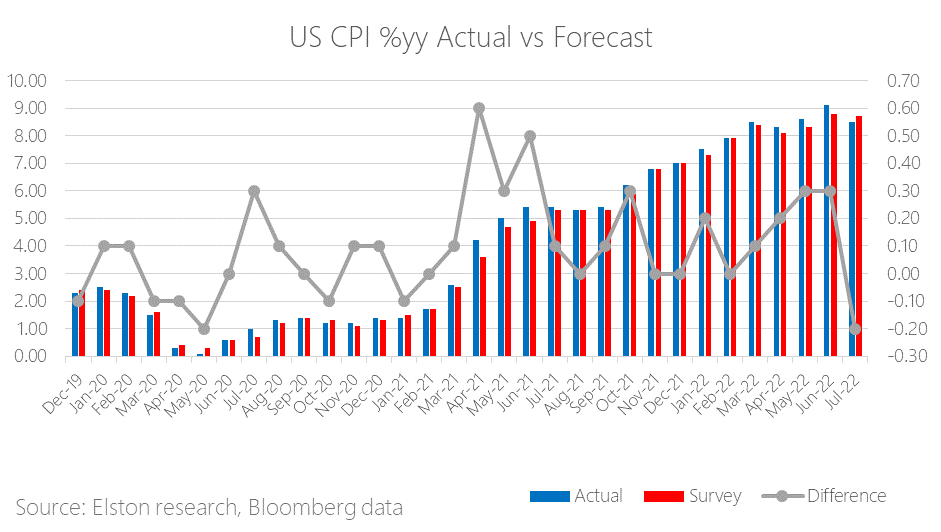

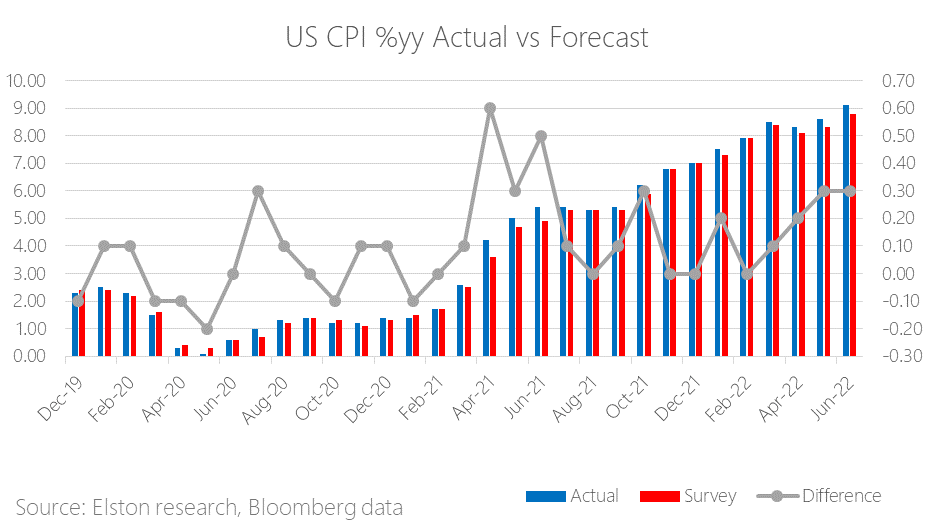

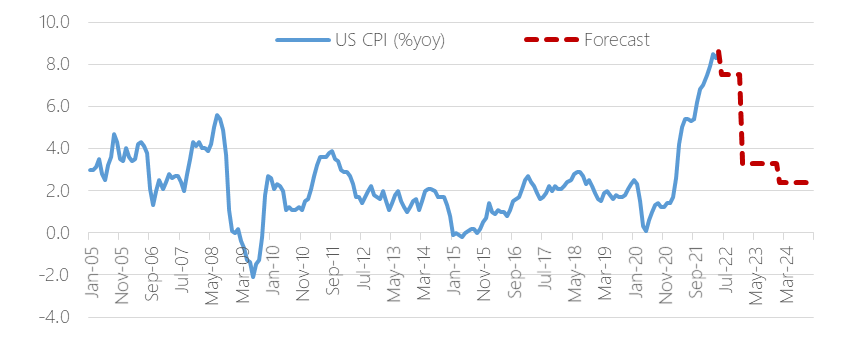

Latest US inflation figures The latest US inflation came in at 8.5%yy for July 2022, lower than survey estimate. This is down from 40-year high of 9.1%yy last month and is lower than expectations of 8.7%. Gasoline prices fell by 7.7% in July, compared to an increase of 11.2%yy in June 2022. Food prices continued rising at a fast rate of 10.9%yy. Shelter cost moved higher by 0.5% from last month and went up by 5.7% from the same time last year. Read in full including charts  [3 min read, open as pdf]

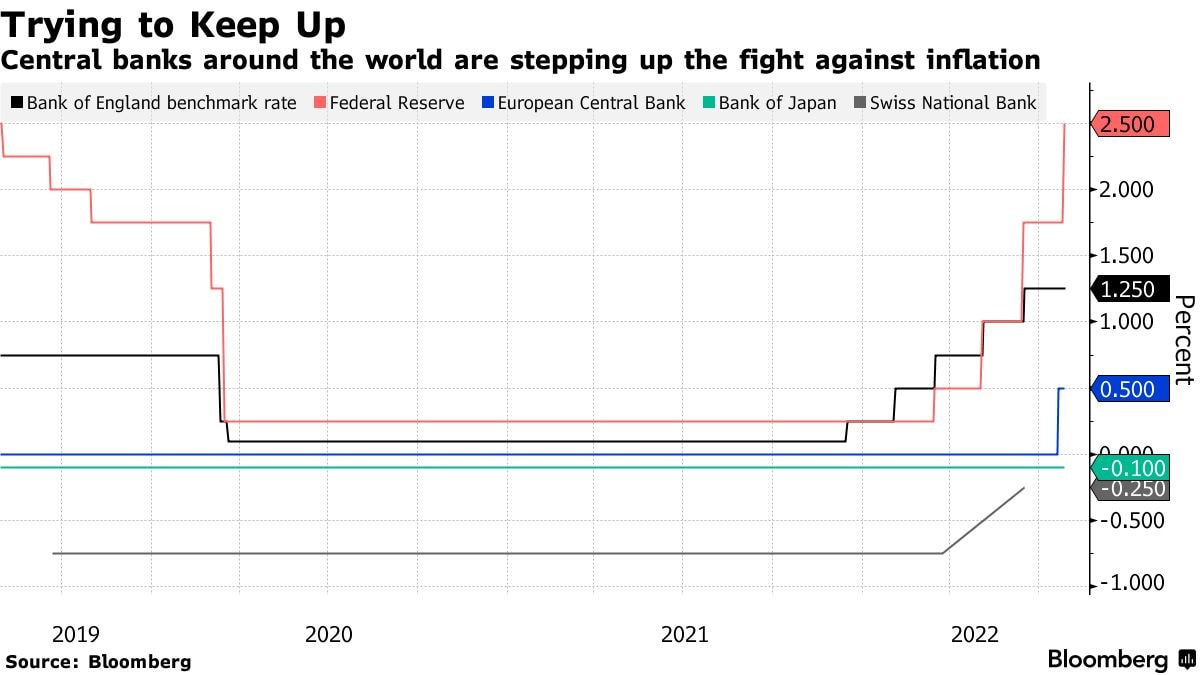

On 4th August, the Bank of England raised rates by 0.5%, the largest single increase since 1995. This followed the US Federal Reserve raising rates by 0.75% at the end of July. While these rate rises may or may not bring inflation under control, the risk they pose to growth is considerable. We consider the ways in which investors can use ETFs to build defensive resilience as an alternative to low-yielding cash or bonds.  [3 min read, open as pdf]

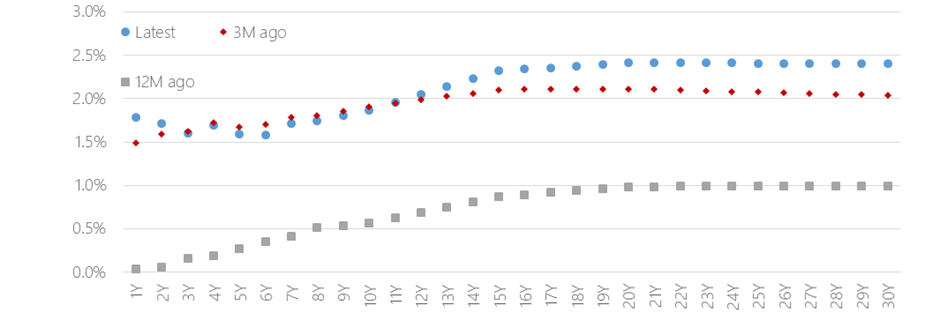

What is the yield curve and how does it illustrate future expectations for the economy? In this article, we explain how to read the yield curve and discuss what the current version is suggesting in terms of inflation, interest rates and recession.  [3min read, open as pdf]

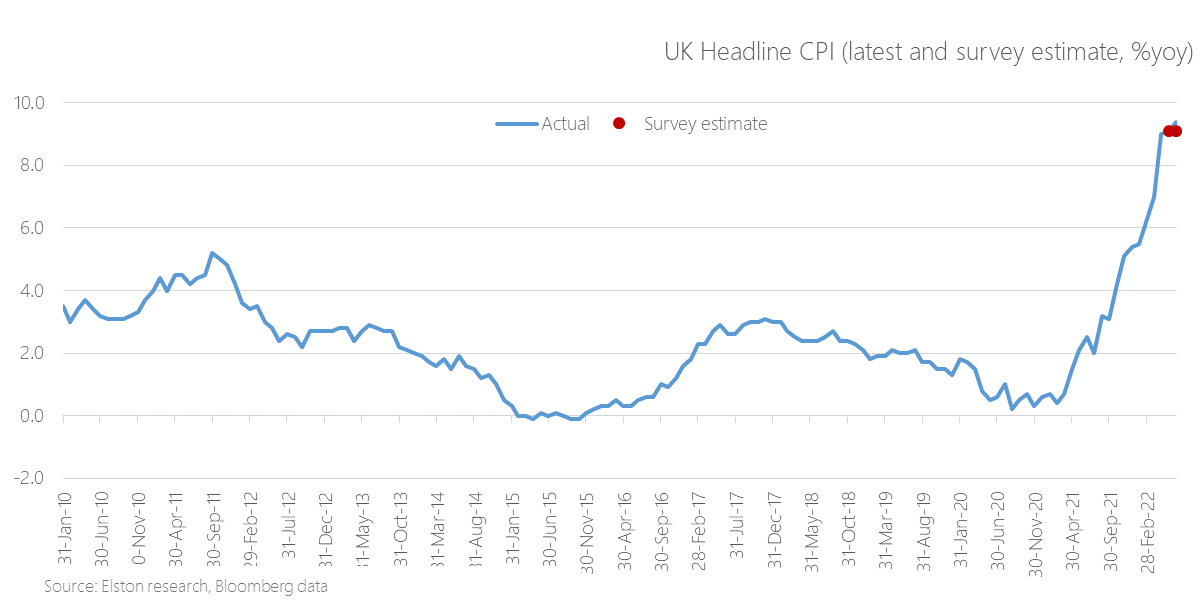

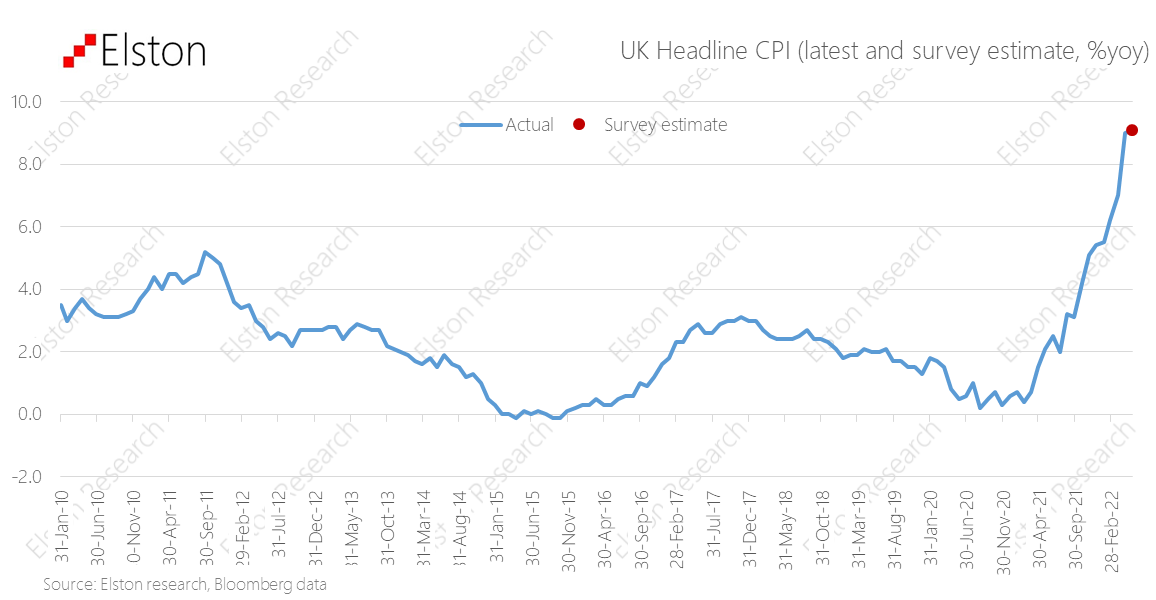

This is the highest UK inflation rate in 40 years. Higher prices for motor fuel and food explained the increase in prices  [5 min read, open as pdf for full article]

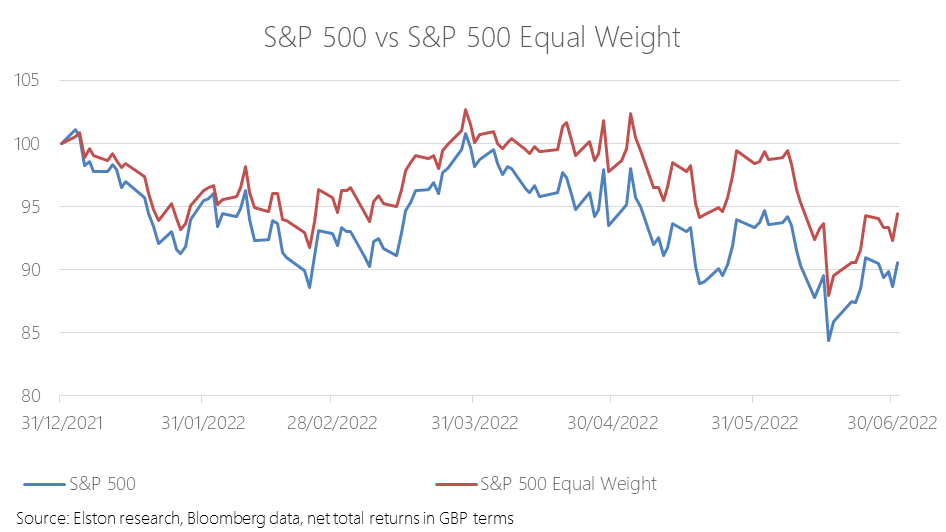

Critics of tracker funds often flagged concentration risk or the “big get bigger” approach of passive investing as a structural flaw to index investing. But concentration risk is a choice, not an obligation for the index investor. As would be expected, an equal weight approach has proved relatively more defensive in the down-market year-to-date. The S&P500 Equal Weight index has returned -5.2% against the traditional S&P 500’s -9.3% YTD, in GBP terms. For more on this topic, please see our CISI-endorsed CPD webinar: The curious power of equal weight, with guest speaker Tim Edwards, Managing Director, Index Investment Strategy, S&P Dow Jones Indices  [3 min read, open as pdf]

Gasoline prices jumped by 11.2% compared to May 2022. Higher prices of food and shelter also contributed to the highest US inflation rate in 40 years. Inflation pressure is broadening as energy and groceries prices surge.  [5 min read, open as pdf]

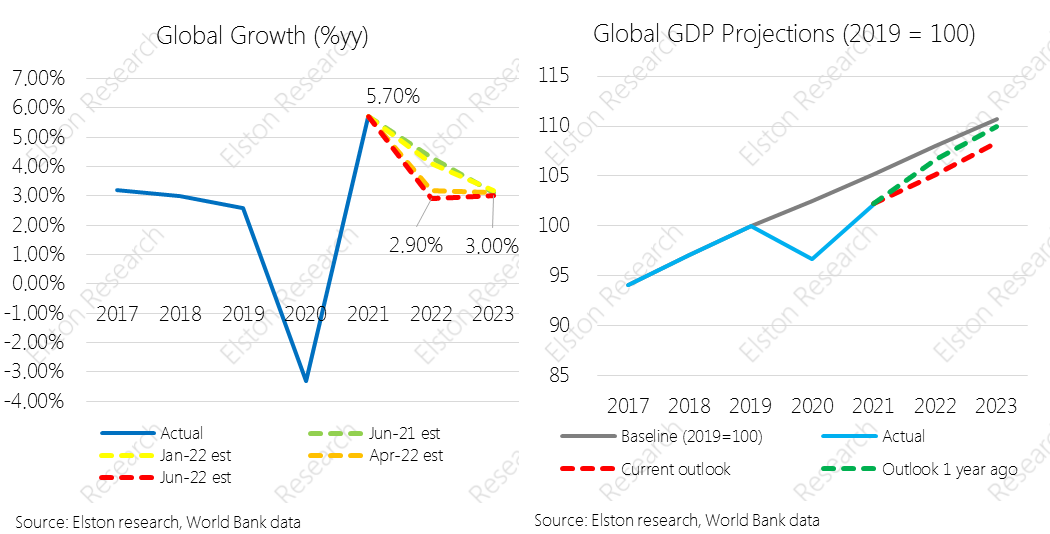

A perfect storm of events is giving rise to the gloomiest global economic outlook since the 1970s. Supply chain disruption brought about by the Covid-19 pandemic has collided with a spiral in energy and commodity prices triggered by the Ukraine war, unleashing a bout of persistently high inflation. Central banks have been slow to react, sticking to their line that the inflation was transitory, meaning that they are now faced with the finest of tightropes to walk between curbing inflation and triggering recession. The World Bank has been steadily revising down its 2022 global growth estimates over the last 12 months. From +4.3%yy in June 2021, to +3.20% in April 2022 to +2.90% in June 2022. For full article, open as pdf  As an investment consultant, a lot of what we do for financial advisers & DFMs we work with is to use our research & development capabilities across Portfolios, Fund & Indices to support our clients' own "proposition development", that goes beyond just portfolio design.

So we were delighted that both our Custom Portfolios solution for advisers - with Elston Portfolio Management - and our Liquid Real Assets Index strategy for inflation protection were "Highly Commended" in the "Best Proposition Development - Overall" Category at the 2022 Investment Week Innovation & Marketing Awards against some very well respected colleagues and providers! We were also very happy to be a Finalist in the "Best Thought Leadership - Retail" category for our extensive CISI-endorsed CPD webinar programme. We would be delighted to work with UK advisers to support your investment proposition, please get in touch if you would like an initial consultation. With inflation at current levels, nominal bonds will remain under pressure. We explore the more resilient alternatives within the bonds universe as well as property, infrastructure, liquid real assets and targeted absolute return funds.

For full article, see Trustnet.  [3 min read, open as pdf]

This is the highest UK inflation rate in 40 years. Higher prices for energy, motor fuel, and clothing explained for half of the increase in prices. Inflation pressure is not yet peaked with Bank of England expecting 11% in 4q22 and a further step-up in the retail energy price cap.  [5 min read, open as pdf]

Markets entered panic mode this week on fears, that all three “macro” factors – Growth, Interest Rates and Inflation – are all heading the wrong direction.

Full article, open as pdf  [5 min read, open as pdf]

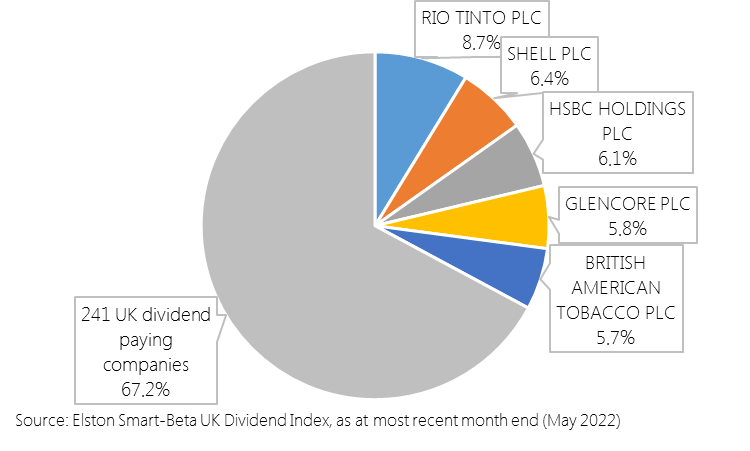

Each quarter we are publishing the Top 5 holdings of our Elston Smart-Beta UK Dividend Index. These are the UK’s largest dividend payers as a proportion of the total dividend pool. For full report open as pdf  [5 min read, open as pdf]

The latest US inflation came in at 8.3%yy for May 2022, higher than survey estimate. This is up from 8.3%yy last month, and is topping expectations. Gasoline prices jumped by 49% compared to May 2021. Higher prices of food and shelter also contributed to the highest US inflation rate in 40 years. Inflation pressure is broadening as energy and groceries prices surge. [For full article and charts, open as pdf]  [5 min read, open as pdf]

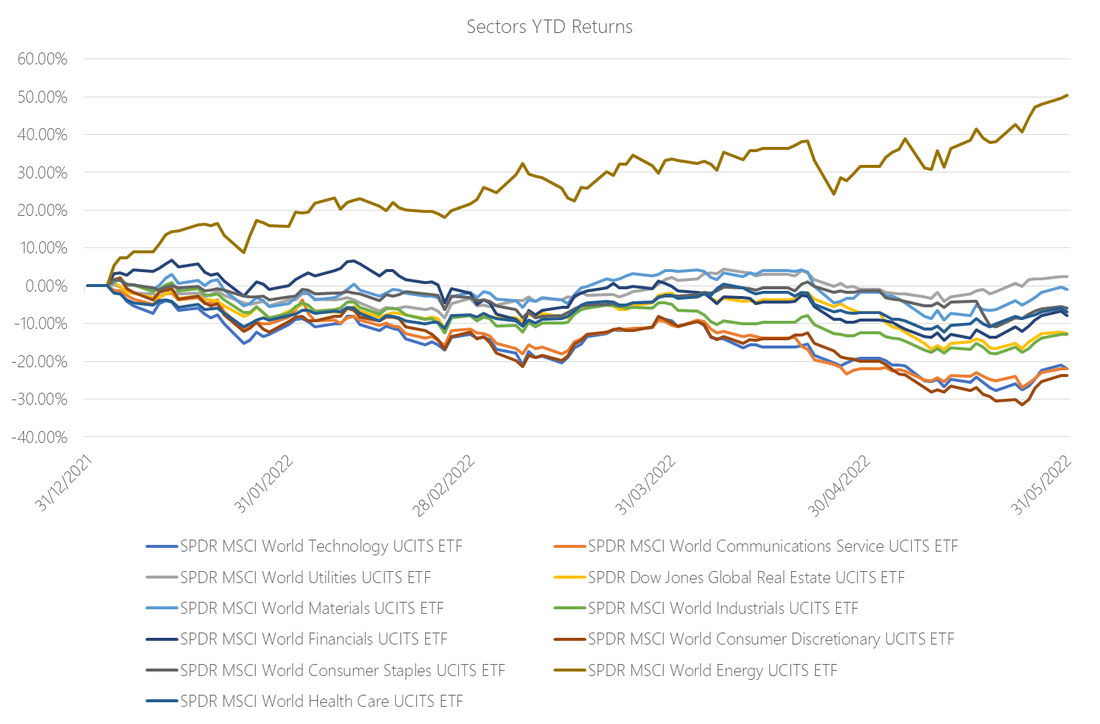

The uncertainty of the current market environment is prompting a pivot away from sectors that have served investors well, in many cases since the financial crisis but particularly during the Covid-19 pandemic. With inflation rampant, commodity prices spiralling, supply chains choked and the much relied-on ‘Fed Put’ (whereby central banks rescue markets by flooding them with liquidity) a thing of the past, investors are rotating away from Technology and Real Estate and into traditionally “boring”, but dependable sectors like Industrials, Materials and Energy. For full article, see pdf  [5 min read, open as pdf]

Read full article with charts  [5 min read, open as pdf]

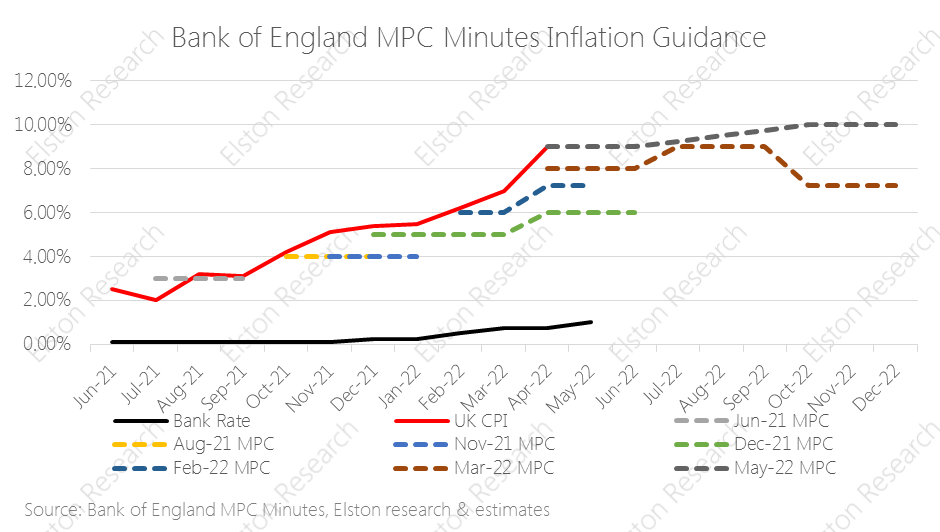

Inflation hits 40 year high UK inflation figures came out today with a print of +9.0%yy (April), from +7.0% (March) and slightly below +9.1%yy consensus estimate. This is the highest level in 40 years, putting renewed focus on the “cost of living crisis”. Rising energy and food costs are the primary drivers, linked to the sanctions regime and the Russia/Ukraine war. The Bank of England has been “behind the curve” as regards to inflation risk. A look at inflation guidance contained in recent Monetary Policy Committee (MPC) minutes shows. Near-term inflation guidance has consistently under-estimated inflation since August 2021 – rising from “above 2%”, to 4%, 6%, 8%,, 9% and now 10%. Read full article with charts  [5 min read, open as pdf]

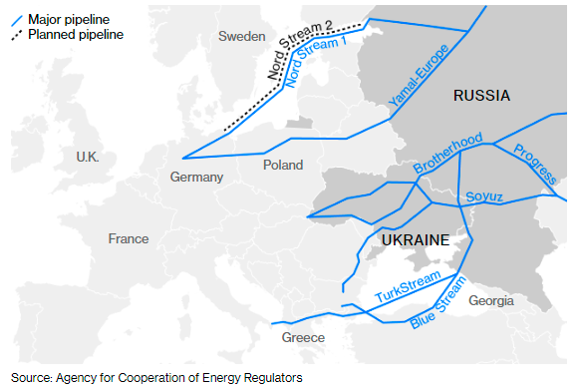

As a result of the Russia/Ukraine war, there is a political goal to reduce European dependency on Russian oil and gas supplies and to reduce the indirect financing of the Russian economy. We explore this topic further in conversation with Nadia Kazakova of Renaissance Energy Advisors.  [5 min read, open as pdf]

Should equity returns be hedged into investor’s base currency? We don’t think so. From a UK perspective, part of the risk-return opportunity of global equity investing is a diversified revenue stream from multiple currencies. Read full article as pdf  [5 min read, full article in pdf]

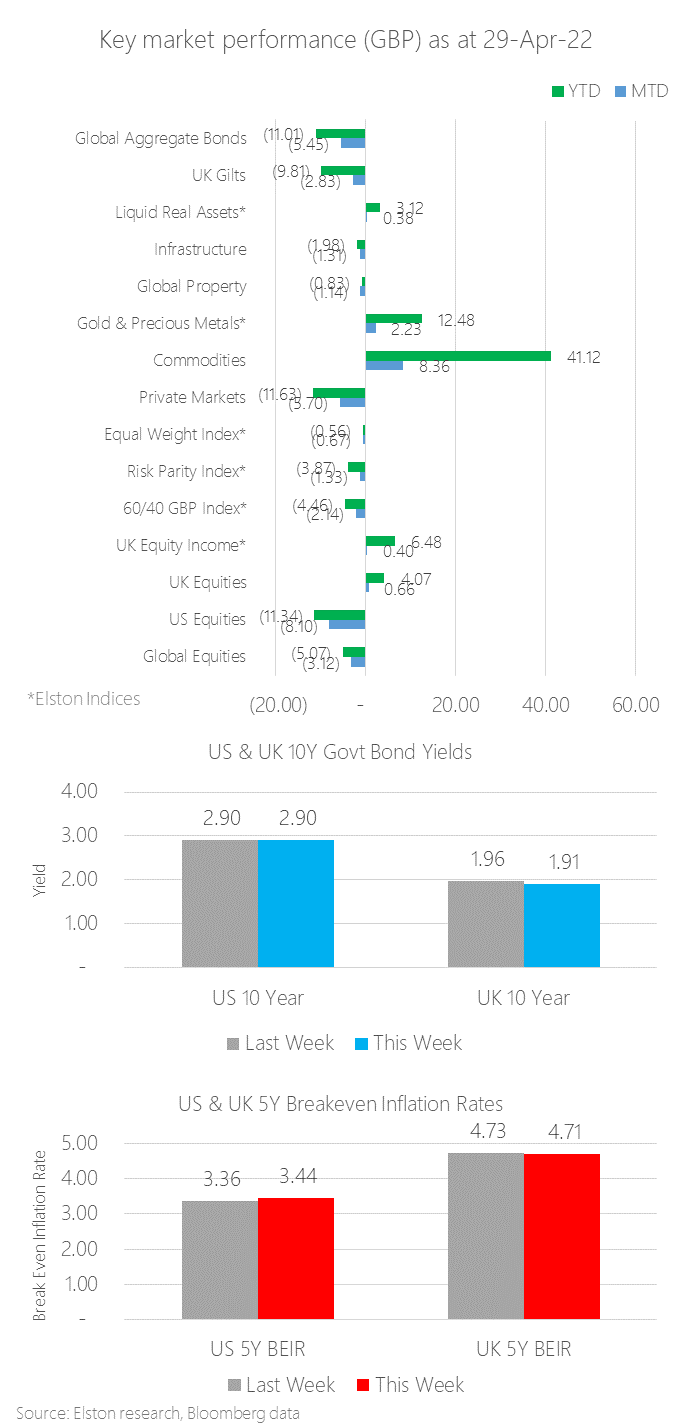

Monthly update, by exposure Once again, Commodities were the top performing asset class in April, returning +8.36% in GBP terms, owing to ongoing inflation pressure from the Russia/Ukraine war, supply-chain, sanctions and energy crisis. Gold & Precious Metals returned +2.23% as an inflation hedge. UK Equities were up +0.66%, and UK Equity Income +0.40%, compared to -8.10% for US Equities and -3.12% for Global Equities, in GBP terms. UK Equities performance was not an indicator of underlying strength, but a function of the translation effect of overseas revenues, in the context of a dramatic -4.37% decline in Sterling vs the USD – the worst decline since COVID March 2020. This came on the back of weaker retail sales and low consumer confidence. Without government spending to fill a growing vacuum, the cost of living crisis (which will only get worse in the autumn) could become recessionary in nature as consumers and businesses defer spending. This risk to growth is greater than the risk of persistently high government debt levels, in our view. Bonds continued to show they offered no place to hide with Global Aggregate Bonds down -5.45%. Our Liquid Real Assets index returned +0.38% for the month, compared to Gilts -2.83%, with comparable volatility. Within the multi-asset space, our Equal Weight index declined -0.67%, and “Equal Risk” (or “Risk Parity” Index_ returned -1.33%, compared to -2.14% for a traditional 60/40 GBP portfolio. US & UK 10 year yields closed at 2.90% (from 2.32%) and 1.91% (from 1.62%) respectively. US & UK 5 year market-implied Break Even Inflation Rates closed at 3.44% (from 3.51%) and 4.71% (from 4.72%) respectively. See full article in pdf  [5 min read, full article in pdf]

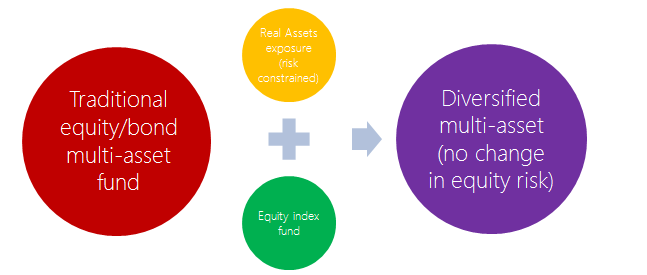

In theory, through 2021 we have argued that bonds would remain under pressure against the twin pressures of rising interest rates and rising inflation. In practice, market dislocations of 1q22 evidenced this as bonds provide no place to hide in a time of market stress, and lost both their diversification and their protection characteristics. Indeed, the losses sustained on the bond side of a traditional multi-asset equity/bond portfolio were more extreme than the losses sustained on the equity side. The pressure on bonds will continue so long as we are in an inflationary regime. And that may be for the medium-term (e.g. 5 or more years based on market implied inflation rates). This is forcing a rethink for advisers reliant on equity/bond multi-asset funds to deliver a core investment strategy for their clients. [Read full article in pdf] Find out more about our Liquid Real Assets index strategy |

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|