[5 min read, open as pdf]

[3 min read, open as pdf]

[5 min, open as pdf]

[5 min read, open as pdf]

The thirty-year anniversary of Black Wednesday was marked by the Sterling reaching its lowest levels against the dollar since 1985. Part of this is a function of dollar strength against global currencies, another part about rising concerns on the UK economic outlook and future policy-making. Sterling’s weakness and outlook is forcing investors to consider how to manage currency risk in their portfolio across each asset class. Full article available as pdf  [3 min read, open as pdf]

[3 min read, open as pdf]

[3 min read, open as pdf]

[3 min read]

[5 min read, open as pdf]

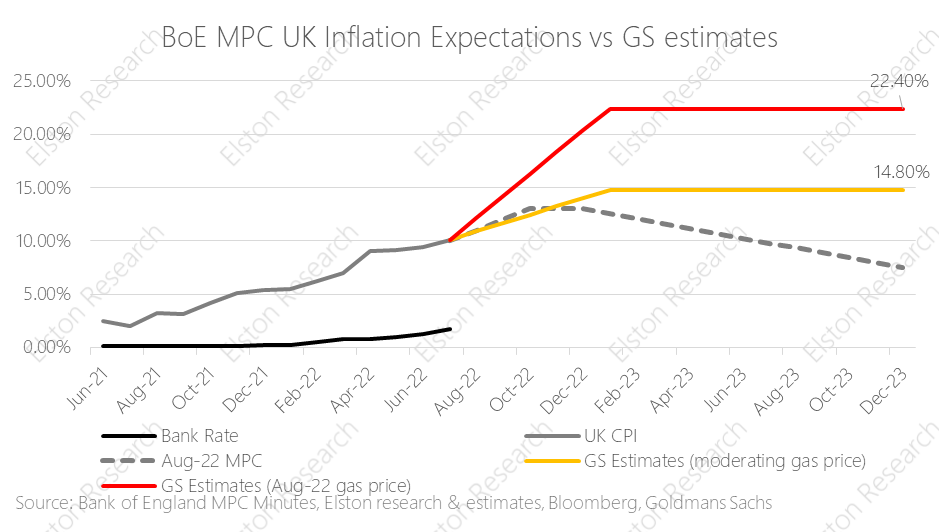

With low growth, soaring inflation and spiking interest rates, advisers need to rethink the definition of risk. Focus on volatility is focus on the “wrong problem”. Instead, advisers should focus on preserving purchasing power (mitigate inflation risk) to protect client outcomes. That requires a fundamental rethink around traditional definitions of risk, asset allocation and diversification. For full article including charts, open as pdf  [3 min read, open as pdf]

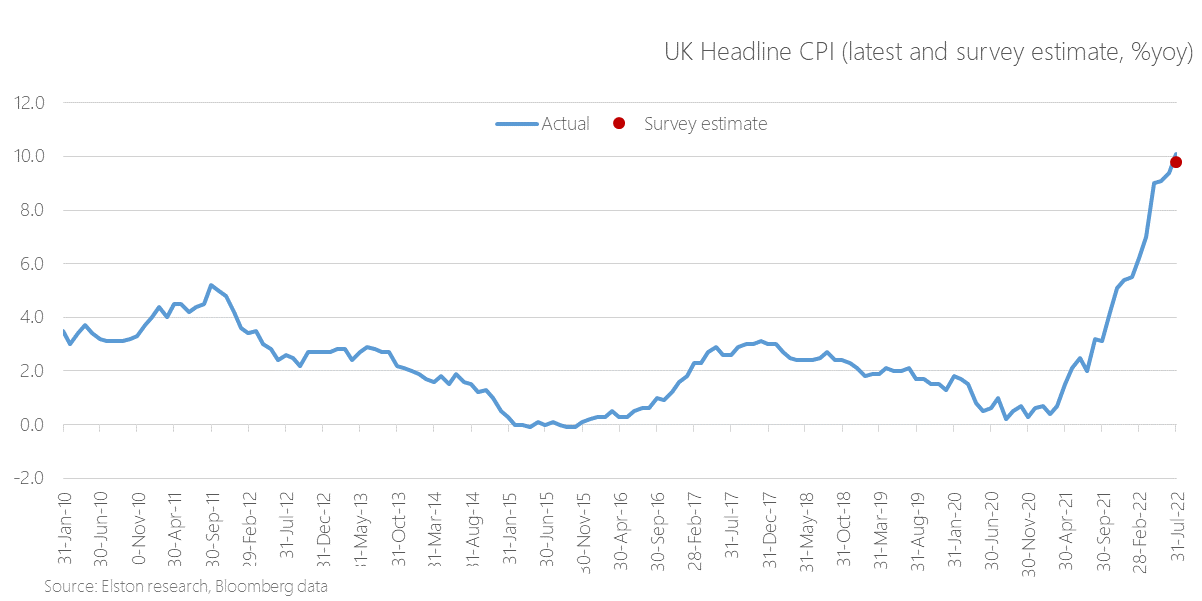

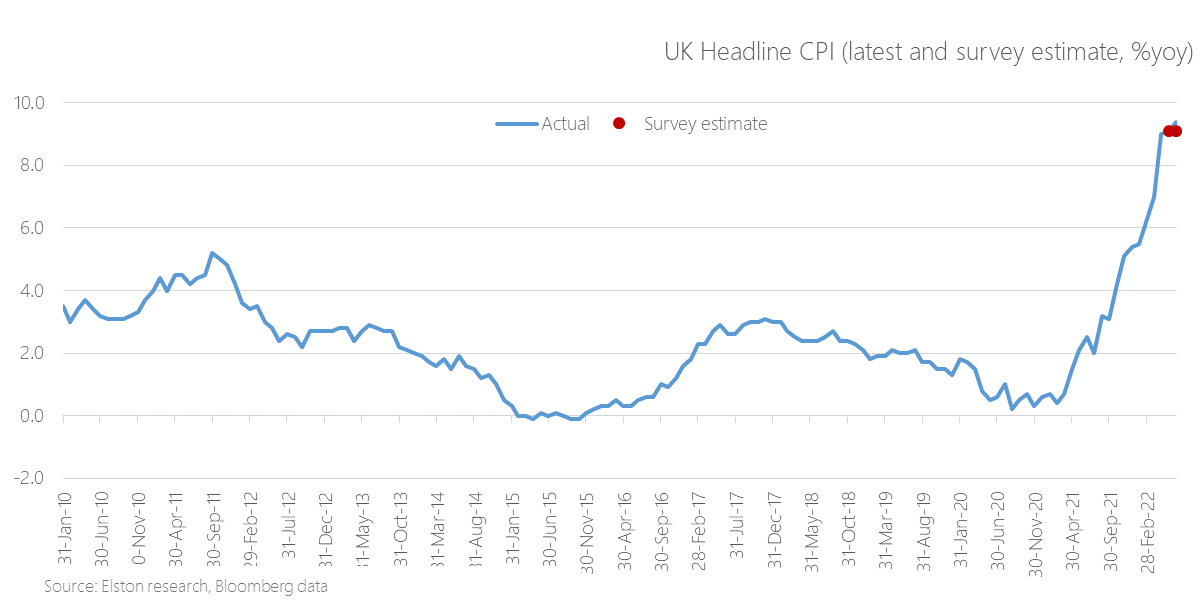

Latest UK inflation figure The latest UK inflation came in at 10.1%yy for June 2022, compared to 9.3%yy survey estimate. This is up from 9.4%yy last month and is above expectations. This is the highest UK inflation rate in 40 years, and now in double digits. Food prices rose meaningfully, especially bakery products, dairy, meat and vegetables, and this was also reflected in higher takeaway-food prices. Inflation pressure has not yet peaked with Bank of England expecting 13% in 4q22 (from 11%) and a further step-up in the retail energy price cap. The BoE remains behind the curve, in our view. See full article including all charts  [3 min read, open as pdf]

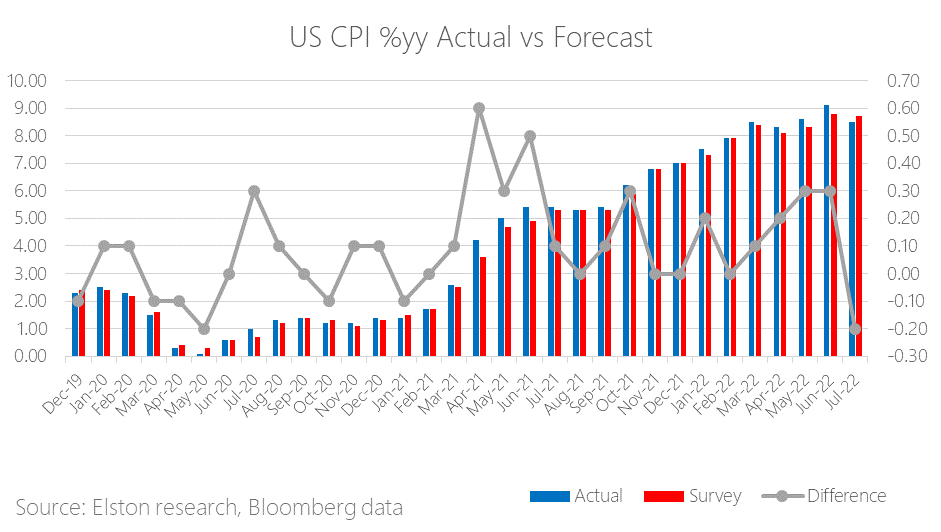

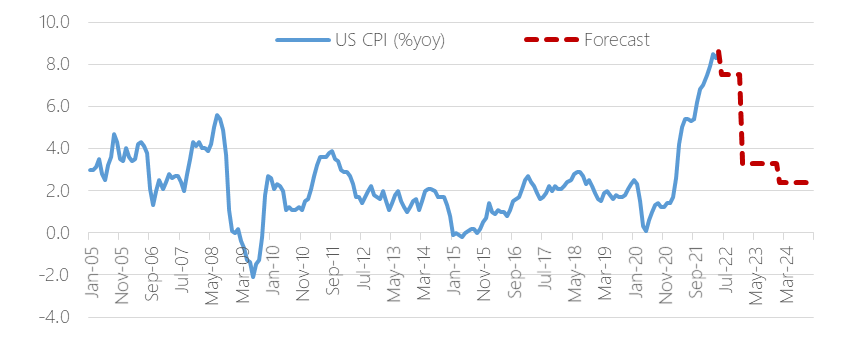

Latest US inflation figures The latest US inflation came in at 8.5%yy for July 2022, lower than survey estimate. This is down from 40-year high of 9.1%yy last month and is lower than expectations of 8.7%. Gasoline prices fell by 7.7% in July, compared to an increase of 11.2%yy in June 2022. Food prices continued rising at a fast rate of 10.9%yy. Shelter cost moved higher by 0.5% from last month and went up by 5.7% from the same time last year. Read in full including charts  [3 min read, open as pdf]

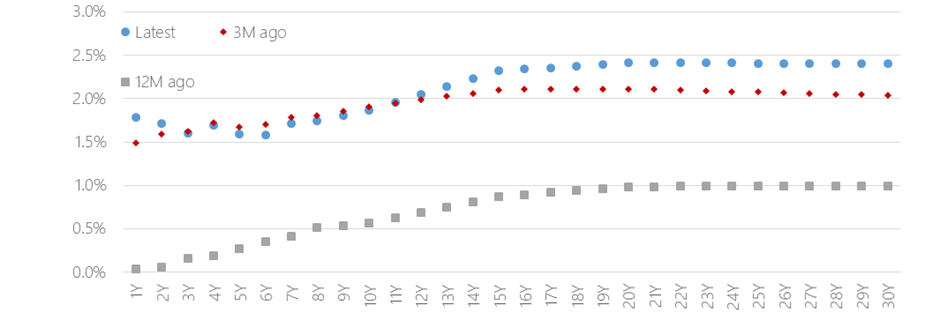

What is the yield curve and how does it illustrate future expectations for the economy? In this article, we explain how to read the yield curve and discuss what the current version is suggesting in terms of inflation, interest rates and recession.  [3min read, open as pdf]

This is the highest UK inflation rate in 40 years. Higher prices for motor fuel and food explained the increase in prices  [5 min read, open as pdf]

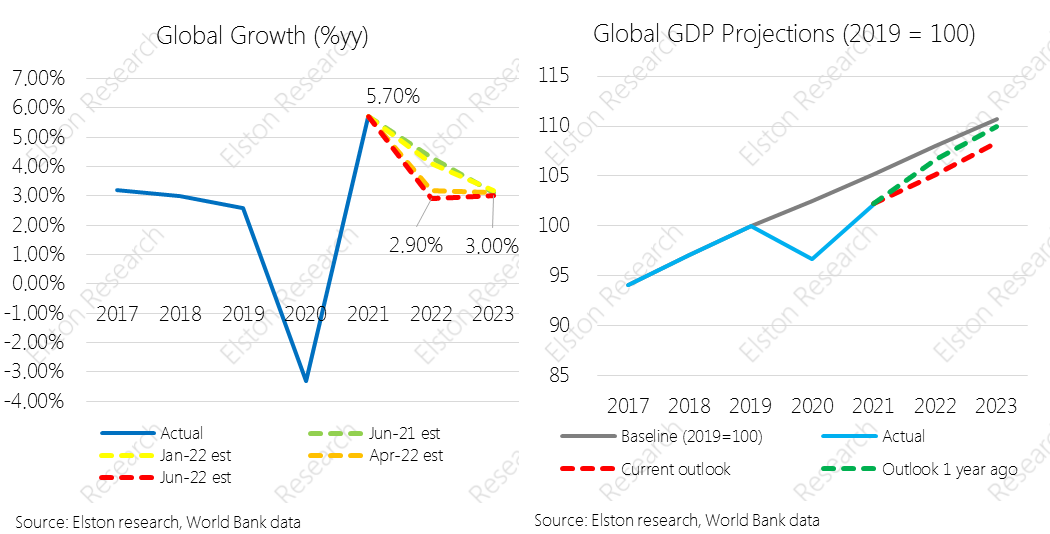

A perfect storm of events is giving rise to the gloomiest global economic outlook since the 1970s. Supply chain disruption brought about by the Covid-19 pandemic has collided with a spiral in energy and commodity prices triggered by the Ukraine war, unleashing a bout of persistently high inflation. Central banks have been slow to react, sticking to their line that the inflation was transitory, meaning that they are now faced with the finest of tightropes to walk between curbing inflation and triggering recession. The World Bank has been steadily revising down its 2022 global growth estimates over the last 12 months. From +4.3%yy in June 2021, to +3.20% in April 2022 to +2.90% in June 2022. For full article, open as pdf  [5 min read, open as pdf]

The latest US inflation came in at 8.3%yy for May 2022, higher than survey estimate. This is up from 8.3%yy last month, and is topping expectations. Gasoline prices jumped by 49% compared to May 2021. Higher prices of food and shelter also contributed to the highest US inflation rate in 40 years. Inflation pressure is broadening as energy and groceries prices surge. [For full article and charts, open as pdf]  [5 min read, open as pdf]

Read full article with charts  [5 min read, open as pdf]

Inflation hits 40 year high UK inflation figures came out today with a print of +9.0%yy (April), from +7.0% (March) and slightly below +9.1%yy consensus estimate. This is the highest level in 40 years, putting renewed focus on the “cost of living crisis”. Rising energy and food costs are the primary drivers, linked to the sanctions regime and the Russia/Ukraine war. The Bank of England has been “behind the curve” as regards to inflation risk. A look at inflation guidance contained in recent Monetary Policy Committee (MPC) minutes shows. Near-term inflation guidance has consistently under-estimated inflation since August 2021 – rising from “above 2%”, to 4%, 6%, 8%,, 9% and now 10%. Read full article with charts  [5 min read, open as pdf]

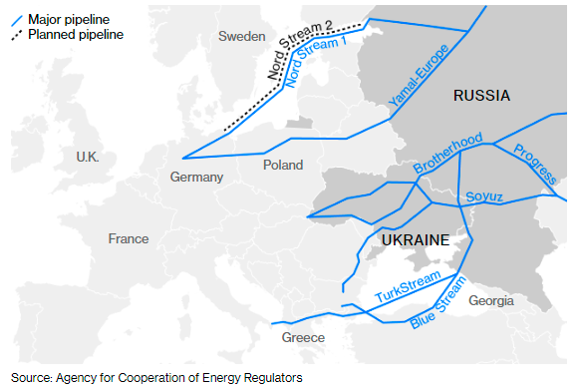

As a result of the Russia/Ukraine war, there is a political goal to reduce European dependency on Russian oil and gas supplies and to reduce the indirect financing of the Russian economy. We explore this topic further in conversation with Nadia Kazakova of Renaissance Energy Advisors.  [5 min read, open as pdf]

Should equity returns be hedged into investor’s base currency? We don’t think so. From a UK perspective, part of the risk-return opportunity of global equity investing is a diversified revenue stream from multiple currencies. Read full article as pdf  [5 min read, open as pdf for full article]

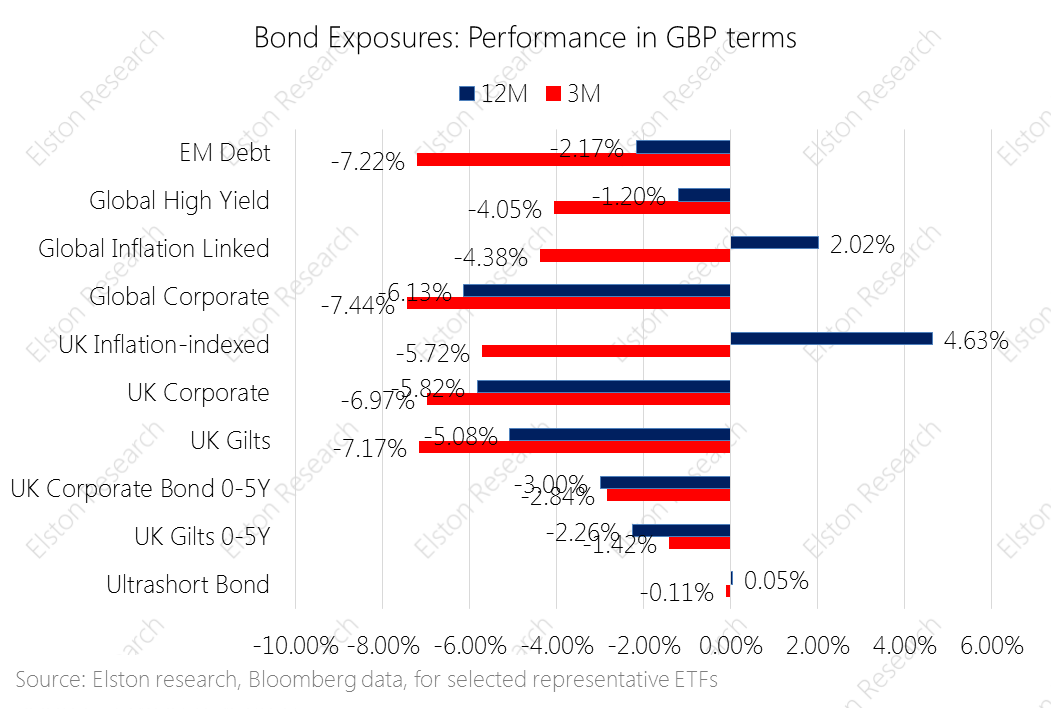

Equity markets endured a triple shock in the first quarter of 2022: a dramatic steepening of the likely path of interests, multi-year high inflation levels and a horrific war unleased in Ukraine. The traditional rational for including nominal bonds was to provide steady income, lower but positive returns, and diversification – a place of safety in periods of market stress. In face of rising inflation and rising interest rates, nominal bonds are providing none of these portfolio functions. Indeed in 1q22 not a single bond exposure delivered positive returns, and over 12 months only inflation-linked exposures delivered positive returns. Open as pdf for full article CPD Webinar Alternatives to Bonds in a Portfolio |

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|